The Trillion-Dollar Shift: Why Embedded AI Agents Will Redefine Finance Before 2030

5 min read | Published

Silicon Valley Bank collapsed in 48 hours. Customers pulled $42 billion in a single day — faster than any bank run in history, not because of panic alone, but because they could. A few taps on a phone moved money while the bank's systems were still processing yesterday's data.

That speed gap is getting worse, not better, and it's forcing fintech to rethink how systems actually operate.

The Problem Nobody Wants to Say Out Loud

Fintech spent the last decade making things look better without significantly changing how they actually work: Slicker apps, prettier dashboards, faster reports, but with the same processes underneath.

That didn't prevent SVB. It doesn't stop the $32 billion lost to payments fraud every year. It doesn't keep portfolios aligned when markets move 3% in an afternoon.

The infrastructure is still the same, decisions wait in approval queues, and risk analysis happens after transactions clear. Rebalancing runs on quarterly schedules that made sense when you had to call your broker.

But markets move in real time, fraud happens 24/7, and customers leave if your system makes them wait while you 'investigate'.

What Production Looks Like Now

Some companies have stopped waiting and instead they're deploying AI agents that investigate and act automatically, without human intervention.

Take fraud investigations, for example. A traditional setup sees the system flag something suspicious, and an analyst spending hours reconstructing logs and merchant histories. By the time action is taken, either the fraudulent action has succeeded or a legitimate customer gets blocked and switches to a competitor.

The new approach investigates the second something looks wrong, traces patterns across the network, checks merchant behavior histories, analyzes device fingerprints, and determines if it's a system error or coordinated fraud. Then it’s either blocked, escalated with complete context already assembled, or approved. No queue. No delay.

False positive rates drop 40-60%. Fraud windows shrink from hours to minutes. When regulators ask why a transaction got blocked, there's a complete decision trail instead of "analyst flagged it."

Or consider portfolio rebalancing. Most wealth platforms still rebalance quarterly because that's how it's always worked. Meanwhile, a client's equity allocation breaches policy after a tech rally, sits out of compliance for eight weeks, and requires expensive tax-loss harvesting to fix what should have been a simple rebalance.

Some systems now continuously monitor every position against a mandate and risk model. If an allocation drifts, the system simulates corrections, calculates transaction costs, and presents options. All this happens with the proper guardrails in place, only executing within approved limits. The knock-on effect means portfolios stay compliant, advisors spend time on relationships instead of spreadsheet maintenance, and fiduciary duty happens in minutes instead of waiting for calendar quarters.

AI Agents are emerging across disclosures, risk reporting, merchant classification, and stress testing. Together, they form a new operating fabric for finance.a

Why Most Attempts Fail

The gap between proof of concept and production is still massive, and most projects stall because they hit one of four walls:

Data that doesn't cooperate

AI Agents need clean, structured, API-accessible data. Your data warehouse might be technically complete, but practically unusable. Structured data in databases, underwriting documents as PDFs, customer communications in email, and compliance files scattered across systems. AI Agents can't work with that kind of fragmentation.

Decisions nobody can explain

When compliance asks, "Why did this system decline this application?" you can't answer, "The model scored it low." You need clear reasoning, traceable data sources, and documented rules. Black boxes don't survive the first audit.

Scale that breaks everything

One agent in testing works fine: What about thousands of AI agents across thousands of customers, each in isolated, secure environments, processing millions of transactions? That's where infrastructure collapses. Most platforms aren't architected for that load.

Security that's bolted on afterward

You can't expose customer financial data to experimental systems, send sensitive information to external LLMs, or have AI agents making decisions in ways you can't audit. If security isn't foundational, the whole thing gets shut down before it reaches production.

What Has to Change

Building systems that actually work in production requires different foundations than building dashboards or reports.

Ontologies, not data lakes

AI Agents need structured knowledge about your business that spans structured datasets and unstructured documents. That means building formal specifications of what things are, how they relate, and what rules apply. When an agent needs to check merchant risk, it shouldn't be parsing PDFs; it should be querying a knowledge graph that already understands your business semantics.

Transparent workflows, not magic

Define exactly what AI agents can do, when they escalate to humans, and what guardrails prevent errors. This isn't about limiting capability — it's about earning trust from compliance teams and regulators who need to understand and audit decisions.

The right tools

LLMs excel at understanding intent, writing summaries, and generating code, but they're terrible at basic logic or anything requiring strict determinism. Decide what actually needs LLM capability — with the cost and data exposure that brings — versus what can run on cheaper, fully deterministic systems. You can build portfolio rebalancing that never exposes holdings to external models; inventory optimization that doesn't hallucinate about stock levels; and production planning that follows procedures exactly.

Embedded at scale

AI Agents must plug directly into production systems — payments, CRMs, trading platforms — and scale without breaking under real-world load.

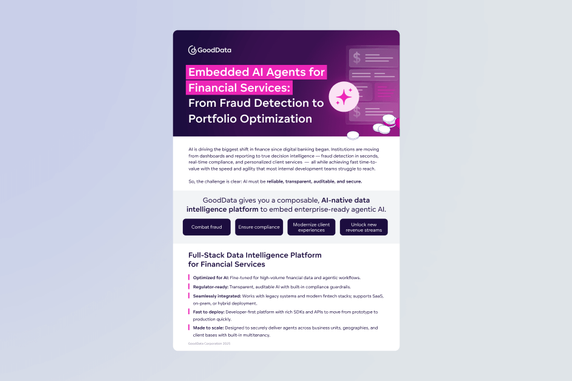

AI Transformation Playbook for Financial Services and Fintech

The key ares to consider in your transition to AI.

Read more

What This Means for Fintech

Traditional banking can afford to move slowly; fintech can't. You're competing on speed and experience. When a customer hits fraud friction with your platform, they switch, and when your wealth product can't keep portfolios optimized, advisors move to competitors.

The fintech companies pulling ahead aren't doing it with better dashboards; they're automating what used to require human review. Not because it's cheaper — though it is — but because it's faster and better. The result is fraud being resolved in seconds instead of hours, portfolio adjustments in minutes instead of quarters, and underwriting decisions being made while customers are still filling out applications.

This isn't about distant future speculation; it's happening now. Some competitors are already running these systems in production, and the advantage compounds — they're building operational experience and customer expectations that will become harder and harder to match later.

Where to Start

For boards and CFOs, the path forward is clear:

Pick one high-value process

An area where automation is both valuable and safe. Something like fraud investigation, reconciliation, or risk scoring, where the metrics are clear and the downside is manageable if something breaks.

Build governance from day one

Define what agents can do automatically, what needs approval, and what's prohibited: Avoid retrofitting guardrails after you've already built everything.

Integrate into real workflows

Connect to payment systems, databases, and CRMs because agents living in sandboxes simply aren't useful; they need to be embedded where the work happens.

Prove it works, then expand

Avoid trying to automate everything simultaneously. Instead, get one process working, measure results, then move to the next.

Build on the Right Foundation

None of this is possible without proper infrastructure. At GoodData, we’ve built an AI-native data intelligence platform designed for production: one foundation that brings together governed semantics, transparent workflows, and scalable deployment. That’s what makes it possible to build limitless embedded agents that are explainable, secure, and ready for enterprise scale.

After years in embedded analytics, we've seen what breaks when you go from pilot to production scale. Whether you want to start with a template or build something custom for your specific use case, we can help you build agents that handle fraud investigation, portfolio rebalancing, risk reporting, and more.

To prepare for your transformation to AI, read our playbook, or to see how GoodData can help you build agents that work in production, request a demo.